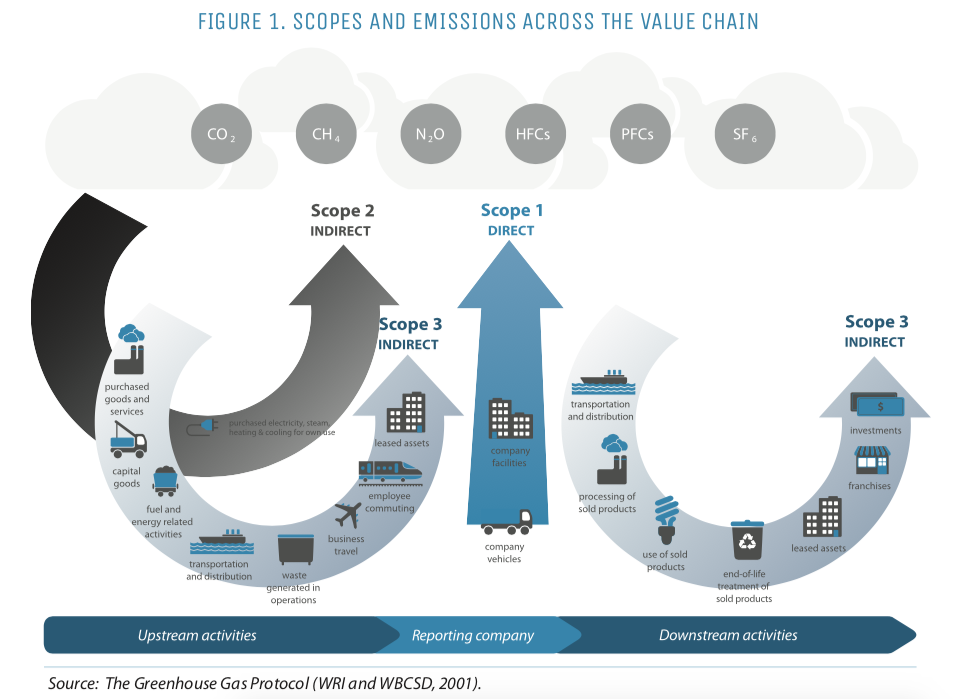

Climate change poses a number of risks to food and agricultural companies that impact their corporate performance and long-term value creation. Land use change (LUC) from commodity crop and subsistence agriculture, particularly in Latin America and Southeast Asia, where the production of beef, soy, palm oil and cocoa have led to 87 percent of all tree cover loss between 2001 and 2015, have an outsized impact on greenhouse gas emissions (FAO, 2016). Of the emissions generated by food systems, most—over 80 percent—stem directly from agricultural production and its associated land-use change (Vermeulen et al., 2012). For most food and agricultural companies, these emissions are considered “scope 3” emissions: upstream or downstream emissions not under direct control of the company (i.e. indirect emissions) (Figure 1). While many companies have for some time estimated and reported greenhouse gas emissions (GHG) from company facilities, company vehicles and purchased electricity (i.e. scope 1 and scope 2 emissions), companies are increasingly recognizing the importance of also measuring and disclosing their scope 3 emissions.

Measuring emissions from agricultural production and LUC within corporate value chains is both essential and difficult. Agricultural emissions are driven by complex interactions between natural and human processes, and estimating these emissions with any accuracy requires data on agricultural management, soil, and climatic factors at the site of production. For a company producing multiple products and sourcing from potentially thousands of producers, collecting such data can be daunting.

This report provides an overview of available resources (i.e. standards, methodologies, tools, and calculators) for assessing emissions from agricultural production and agriculturally-driven LUC. Resources were assessed in terms of how they could help companies track progress on reduction targets for agricultural emissions. The collection of tools and approaches included in this report was assembled from: company reports to CDP; conversations with companies attending a March 2018 workshop on metrics for climate-smart agriculture hosted by the World Business Council for Sustainable Development (WBCSD) and the CGIAR Research Program on Climate Change, Agriculture and Food Security (CCAFS); conversations with service providers in the GHG accounting field; published reviews of agricultural GHG accounting tools; and the authors’ previous knowledge. The report is limited to tools and approaches specific to agricultural commodities, with a limited discussion on the most widely used frameworks for corporate GHG inventories generally.